Lenders can do more to help consumers build better credit card habits, an ASIC report reveals.

Credit card lending in Australia: Staying in control (REP 788), looked at around 20 million credit card accounts across 13 lenders over six years.

ASIC Commissioner Kate O'Rourke said, "While many Australians have changed how they use credit cards, there are still lots of Australians, particularly younger ones, who continue to struggle with credit card debt.

"We recognise that lenders have come some way in taking proactive steps to address persistent debt, low repayments and poorly suited products.

"The product design and distribution obligations, introduced in 2021, have been a contributing factor, as they require firms to design financial products that meet consumer needs, while distributing products in a more targeted way.

"This report identifies practical ways that lenders can do more to support their customers."

Commissioner O'Rourke highlighted actions credit card lenders could take to improve consumer outcomes, identifying a number of better practices some lenders had implemented.

These included:

- providing alternative account options for those who have problematic debt

- excluding consumers with problematic debt from marketing campaigns

- providing consumers with targeted reminders and education to help reduce persistent debt

- promoting credit card selector tools and conducting ongoing assessment of those using high-interest cards

- adopting measurable review triggers, including consumer outcomes, to enhance target markets, and

- analysing data so those at risk of financial hardship may be identified sooner.

"It is encouraging to see that credit card providers have upheld many commitments made following our 2018 review, with some making further inroads," Commissioner O'Rourke said.

One participating lender trialled sending SMS reminders to encourage consumers with problematic debt to make repayments earlier and pay more than the minimum amount. This resulted in a 28% increase in payments.

On the other hand, some credit card providers failed to analyse their own data to identify consumers who may be at risk of financial hardship and communicate what help may be available.

"Our findings also indicated that many consumers are still on high interest rate cards and could have saved over $468 million during the six-year-review period if they were on low interest rate cards," Commissioner O'Rourke said.

"Some consumers may choose high interest rate cards for particular features and benefits. However, this figure emphasises why credit card selector tools and ongoing assessments by lenders are important to ensure consumers have credit cards and credit card features that best suit their needs, objectives and financial situation."

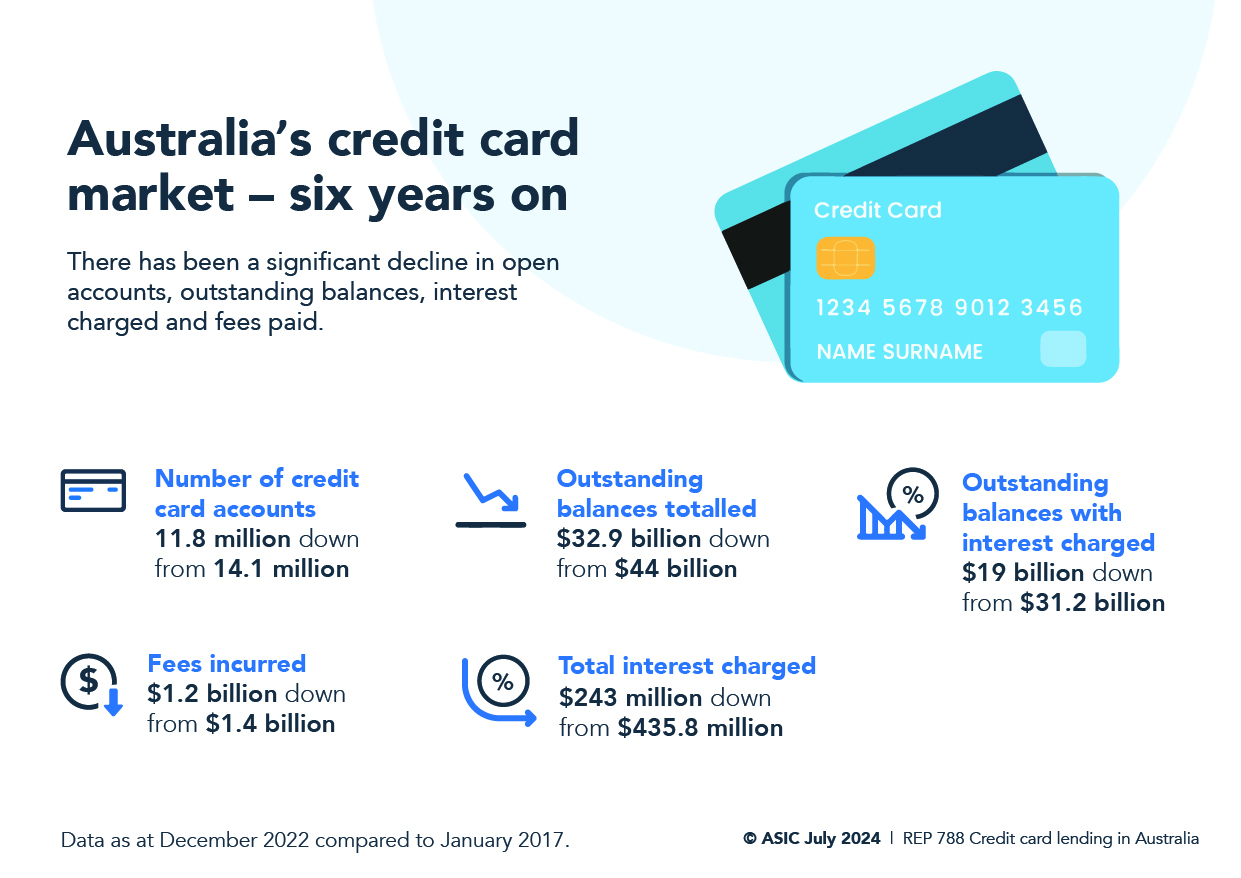

Over the review period, there was a significant decline in problematic debt, as well as the number of credit card accounts, total outstanding balances, amount of interest paid and fees charged.

"The impact of the pandemic, subsequent responses by government and industry, and evolving market conditions certainly played a role in these declines over the period," Commissioner O'Rourke said.

Snapshot of the market

Australia's credit card market - six years on - infographic text version

There has been a significant decline in open accounts, outstanding balances, interest charged and fees paid.

- Number of credit card accounts: 11.8 million down from 14.1 million.

- Outstanding balances totalled: $32.9 billion down from $44 billion.

- Outstanding balances with interest charged: $19 billion down from $31.2 billion.

- Fees incurred: $1.2 billion down from $1.4 billion.

- Total interest charged: $243 million down from $435.8 million.

Data as at December 2022 compared to January 2017.

ASIC's review

REP 788 contains data collected by ASIC between 1 January 2017 and 31 December 2022. To improve the currency of the report, this data was supplemented by data up to May 2024 from the Reserve Bank of Australia (RBA), Australian Bureau of Statistics and the Australian Prudential Regulation Authority.

The recent data, including the statistics from the RBA, indicated that there has been no significant increase in the number of open credit card accounts. Spending and total outstanding balances on credit cards have increased slightly since the review, but the total amount of credit card debt accruing interest has remained flat.

The 13 lenders in ASIC's review represented the vast majority of the Australian credit card market:

- American Express Australia Limited

- Australia and New Zealand Banking Group

- Bendigo and Adelaide Bank

- Citigroup Pty Ltd

- Commonwealth Bank of Australia

- Great Southern Bank (a business name of Credit Union Australia Ltd)

- HSBC Bank Australia Limited

- Humm Group Limited

- ING Bank Australia

- Latitude Personal Finance Limited

- Macquarie Bank Limited

- National Australia Bank, and

- Westpac Banking Corporation.

Background

On 4 July 2018, ASIC published Credit card lending in Australia (REP 580). This looked at credit card lending practises between 2012 and 2017 and identified issues with product design and sales that resulted in consumer harm.

On 18 December 2018, ASIC published Credit card lending in Australia-An update (REP 604). This outlined what credit card providers had committed to and next steps.

Separate to this latest review, ASIC took action against American Express Australia (Amex) for alleged breaches of the design and distribution obligations of their co-branded credit cards, primarily distributed through David Jones stores. On 19 July 2024, the Federal Court of Australia ordered Amex to pay $8 million in penalties.