South America continues to build momentum, with improving market access, growing herds and undervalued currency favouring exports. These conditions will continue to support beef export growth off the back of a strong start to 2019.

Year-to-July beef exports from the big four South American producers (Brazil, Argentina, Paraguay, Uruguay) have well surpassed 2018 levels, currently sitting just above 1.4 million tonnes and tracking 18% above last year.

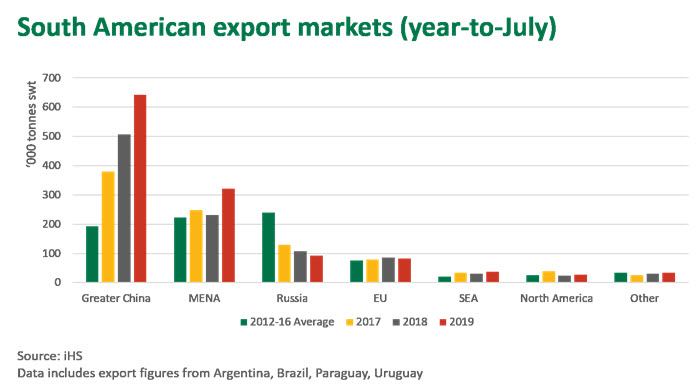

China has clearly gained precedence, with the majority of exports pivoting away from Russia, the regions traditional partner. Year-to-July beef exports to China currently sit just under 500,000 tonnes, up 37% on a year-ago and accounting for 35% of total exports from South America (only 5 years ago this figure was 5%). Demand is expected to keep building heading into the Chinese New Year in January 2020 as African Swine Fever bites into protein supply. Considering the strong global demand for animal protein and the startlingly low value of the Argentine Peso and Brazilian Real relative to the US dollar, South American exports are expected to keep growing.

Despite increasing competition from other nations, Australia still maintains its status as a high-quality and reliable beef producer. As big South American countries continue to build market share through production gains and new trade relationships, it is important to continue analysing how their contribution to the global beef market will affect Australia moving forward.

Market highlights:

Brazil

- Year-to-July exports up 22% on 2018

- Global and domestic pressure weakens the Brazilian real but no recession yet

Brazil has recently had some big market access wins, last month reaching an agreement to supply Indonesia with 50,000 tonnes over the next 12 months (as discussed last week), and a beneficiary of the Mercosur-EU trade deal, negotiations of which concluded in June. However, the deal still needs to be ratified by both sides' parliaments and, complicating things further, and has recently received push back from Ireland regarding the clearing of Amazon rainforest for farmland.

For the year-to-July, Brazilian global beef exports have reached 810,000 tonnes swt. Shipments to China were up 11% on 2018, which is relatively modest when compared to its Argentine (up 103%) and Uruguayan (up 35%) neighbours, who have had the bulk of their product snapped up by China. Meanwhile, Brazilian shipments to Hong Kong are down 10%, greatly affected by higher costs through the grey channel. Reports suggest Chinese interest in Brazilian beef is growing, and higher shipments are expected for August. This interest has been verified with the recent Chinese approval of 17 beef processing plants in Brazil for export.

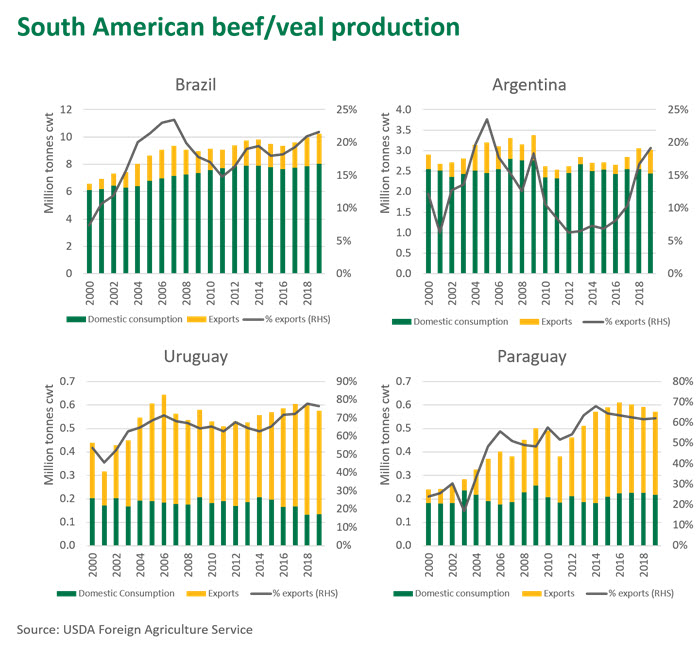

Beef production throughout Brazil continues to increase, with investments leading to improved production efficiency, disease management, and supply chain traceability. Since the beginning of the millennium, Brazil has increased its beef production by 55%, or a staggering 3.7 million tonnes. Much of these production gains can be attributed to the increase in the size of their national herd, growing by almost 17 million head over the course of 20 years.

Argentina

- Year-to-July exports up 44%

- Cow slaughter has been running above year ago levels as strong export prices and local financial pressures have encouraged producers to cull herds

The current economic situation in Argentina is rather delicate and fragile, with ongoing commotion regarding elections. After Mauricio Macrio lost the first round of elections earlier in August, the Argentine Peso has lost 25% of its value relative to the U.S dollar. With high levels of inflation and the Argentine Peso at a historic low, Argentina is sitting at the brink of a financial crisis. The low value of the Peso will continue to make Argentina an attractive supply source for China, while higher levels of inflation will likely slow local beef consumption through 2019.

While Argentina has been granted access to the US, shipments there have been minimal due to the strong demand from China. There is an undoubtable growing dependence on China, which has accounted for 73% of Argentine beef exports this year (195,000 tonnes swt of a total 265,000 tonnes swt).

High interest rates have made business conditions tricky for farmers, with the Argentine cattle herd potentially dropping 400 thousand head next year (cows represented 50.1% of slaughter for the first half of the year).

Uruguay

- Year-to-July exports up 6%

- Strong prices have encouraged liquidation

- Beef production has increased by 137% since 2000

Uruguay has positioned itself well within the market for grass-fed beef, underpinned by strict sanitary standards and excellent transparency along their supply chain. Uruguay is targeting the China market by increasing branding and marketing initiatives, in particular through the southern regions. Current exports for the year-to-July sit at 195,000 tonnes swt, with 68% of this heading to China. With access into a number of key markets (namely the US, China and the EU), Uruguay are a strategic competitor for Australia, but exports are limited by a relatively modest supply base.

For most of 2019 slaughter levels have been sitting above the 5 year average as high prices have encouraged liquidation. Lower cattle inventories and improving weather and feed conditions have slowed slaughter through winter, with August figures down 3,000 head on the same week last year.

Paraguay

- Year-to-July exports down 14%

- Possible recession looming

2019 has been a bumpy year for Paraguay, with flooding in March and May slowing sales, declining cattle prices and a fire at one of the largest meat packing plants reducing slaughter cattle demand. Year-to-July exports sit at 130,000 tonnes swt, with the majority of this beef heading to Russia and other destinations around South America. A projected increase in beef production and slow domestic consumption should lead to a revival of beef exports next year. Cattle slaughter picked up by 2% in August (compared to August last year), which possibly indicates the beginning of improving slaughter pace for the second half of the year.

© Meat & Livestock Australia Limited, 2019

To build your own custom report with MLA's market information tool click here.

To view the specification of the indicators reported by MLA's National Livestock Reporting Service click here.