New Zealand's super for a house scheme is a cautionary tale for Australia, with new research confirming Kiwi house prices spiked and home ownership rates fell after the policy was introduced.

The New Zealand lived experience shows a policy to bust open super for housing would not help first home buyers get into the market in Australia – this real-world example shows home prices rose even faster and homeownership rates fell.

A Super Members Council examination of the detailed evidence from New Zealand shows that since the KiwiSaver HomeStart scheme started in 2010:

- house prices in New Zealand spiked upwards in-line with withdrawals from KiwiSaver

- home ownership rates fell overall, and dropped sharply for people in their 30s,

- Mortgages steeply increased, as did debt levels among first home buyers

Since the policy's introduction there, house prices in New Zealand have risen 134% from June 2010-June 2024, more than in the previous two decades and 1.5 times faster than house prices in Australia.

The policy has not worked. A smaller share of New Zealanders become homeowners since its introduction – particularly among the first home buyer demographic – where ownership has fallen by about 7 per cent for people in their 30s.

Mortgage amounts have also spiked for first home buyers as they are forced to take on eyewatering amounts of debt to keep up with the rising house prices.

Since 2014, the total number of first home buyers taking out loans with a loan-to-value ratio over 80 per cent has tripled, and the proportion of high LVR loans taken out by first home buyers has risen from 25 to 75 per cent.

In a cost-of-living crisis, this means higher mortgage repayments and more financial stress.

As house prices have skyrocketed, accessing their retirement savings is no longer a choice for young New Zealanders – it's a necessity to get into the market.

First home buyers accessing KiwiSaver to buy a home has risen from 65 per cent in 2015-16 to 77 per cent in 2023-24.

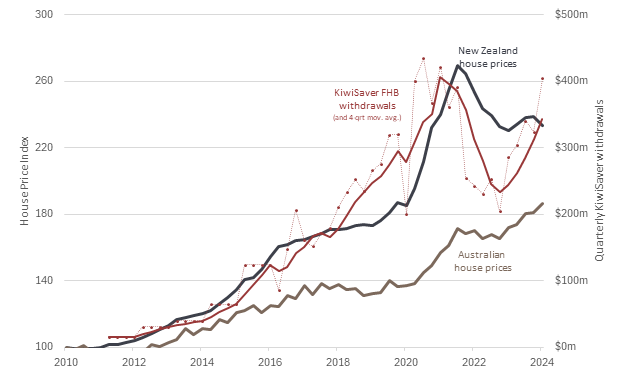

Withdrawals from KiwiSaver are a lead indicator of New Zealand house price movements: when withdrawals increased, house prices jumped - and when withdrawals declined during the COVID period, house prices did too. (See figure 1)

Super Members Council CEO Misha Schubert said Australia should heed New Zealand's cautionary tale and not make the same policy mistake here.

"If you want to see further rises in house prices and falling home ownership rates – New Zealand shows introducing a super for a house policy leads in that direction," she said.

"But if you want to fix the housing crisis, then the answer is building many more new homes to expand supply, rather than telling young people that raiding their super is the answer."

"The evidence is clear – from an overwhelming majority of leading economists and new analysis of New Zealand's real-world experience -that using super for house deposits will just further drive-up house prices, fuel higher mortgages and debt stress in a cost-of-living crisis, and push the Great Australian Dream of home ownership even further out of reach for many young Australians."

The overwhelming majority of Australia's leading respected economists say the housing supply and affordability crisis needs to be tackled with other policies – in a recent Economic Society of Australia survey, only 1 out of 49 top economists supported withdrawals of super for housing.

In a comprehensive report for the Super Members Council, respected independent economist Saul Eslake showed policies that allow Australians to pay more for housing just result in more expensive homes rather than a higher proportion of people owning housing.

To meet the demand for withdrawals for KiwiSaver, New Zealand retirement funds must hold more cash and other liquid assets than their Australians counterparts – leading to lower investment returns.

As of September 2024, Australian MySuper products had outperformed comparable KiwiSaver investment options by an average of 1.16 per cent every year for the previous decade.

If KiwiSaver's lower net returns were replicated in Australia a 30-year-old Australian worker with $25,000 in superannuation today and earning the median Australian wage would be $132,000 worse off at retirement (age 67) in today's dollars.

Government spending in Australia on the pension is falling, while in New Zealand it is increasing. Introducing a super for house policy in Australia would see the cost of Australia's pension system start to rise again, blowing out to a peak of $8 billion per annum – and a total cumulative cost to the Budget of $304 billion by 2102.

Figure 1. New Zealand house prices and KiwiSaver withdrawals